Today, the Hong Kong Stock Exchange disclosed that the e-commerce operator service provider of China’s leading brand e-commerce operator-Youquhui updated the data set after the hearing. This company focuses on providing integrated, omni-channel, high-value-added e-commerce for Japanese FMCG brands. The leading company in the segmented field of operating integrated services may have the opportunity to become The second brand e-commerce listed company in Hong Kong’s capital market .

Last year, according to data from the National Bureau of Statistics, the proportion of national online retail sales in the total retail sales of consumer goods officially exceeded the 20% mark. With the e-commerce dividends over the past decade, China has not only become the world’s largest e-commerce market, but also e-commerce giants such as Alibaba, JD.com, and Pinduoduo have been born in the capital market. The total market value of the three has exceeded RMB 5.5 trillion.

As the e-commerce industry thrives, there are two clearly visible industries: one is the logistics industry, and the other is the brand e-commerce operation service industry that is generally ignored by the market-providing a backstage for the digital business transformation of brand businesses Technical support and front office operations services, etc.

At the end of September last year, the industry leader Baozun e-commerce returned to Hong Kong’s “secondary listing”, or formally started a new wave of tapping the market value of many brand e-commerce companies hidden behind the e-commerce giants, followed closely. Yes, the deep-growing and vertical brand e-commerce companies have also received more attention from the capital market.

The arrival of Youquhui may reopen the window for the reassessment of the brand e-commerce industry.

The scale of revenue is industry-leading, and the pre-IPO valuation has increased rapidly

As a number of Japanese FMCG brands have captured a large number of loyal fans in China, Japan has become the country with the highest annual growth rate among the top five countries of origin in the cross-border online retail market, and the business trend of Youquhui has also increased.

According to the prospectus, Youquhui recorded revenue of 2.8 billion yuan in 2020. From the perspective of revenue growth from 2018 to 2020, the company’s revenue has shown a characteristic of steady growth. The company’s revenue scale in 2020 is comparable 247% of the company (Ruo Yuchen, which is positioned as a fast-moving brand e-commerce company on the A-share SME board), has a significant lead.

Another point of concern to investors is that Youquhui has net losses of 79.495 million yuan and 16.162 million yuan in 2019 and 2020, respectively, but according to the prospectus, the losses are mainly due to changes in the fair value of preferred stocks.

In the rapid growth of some companies, it is very common to issue convertible preferred stocks for financing development. During the rapid growth process, the company’s valuation continues to rise, resulting in a huge “book appreciation” of these preferred stocks. The International Financial Reporting and Accounting Standards require that the “book value increase” of this preferred stock be counted as a loss, which has created the illusion that many high-growth companies have a book “loss”.

To borrow from Kai-Fu Lee, the head of Innovation Workshop, the fair value loss of preferred stocks is not a real loss (here refers to a loss incurred in operation), but includes the value-added of investors. That is, the greater the increase in valuation, the greater the “book loss” caused by the fair value of preferred stocks, and these increasing “losses” are in fact a testament to the company’s rapid growth.

Excluding the influence of factors such as changes in the fair value of preferred shares, Youquhui’s adjusted non-IFRS profits for 2019-2020 should actually be 139 million yuan and 107 million yuan. Judging from the adjusted data, Youquhui’s profitability is relatively healthy, and it has been able to continue to generate relatively stable profits.

The company’s investment value and growth, or the changes in the fair value of preferred stocks shown on its books, have a preliminary “show”. The author is still looking forward to the listing of Youquhui, which will further demonstrate long-term value creation capabilities on the track of rapid growth potential. With the continuous release of performance, the company’s valuation may still have a large room for improvement.

Gross profit margin continues to increase, and internal growth is evident

As the TOP1 existence in the e-commerce operation service field of Japanese FMCG brands, we interpret the revenue structure of Youquhui from two dimensions.

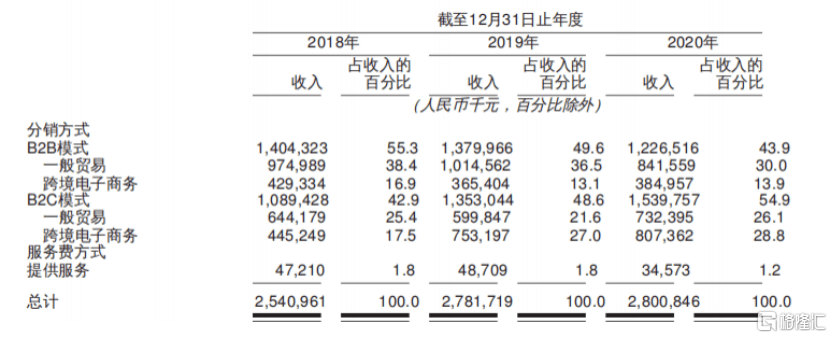

First, it is divided according to the traditional distribution, agency sales and operation business of brand e-commerce. Youquhui’s business income mainly comes from B2B, B2C sales gap and brand operation service fees, of which B2B revenue accounted for 43.9%, B2C revenue accounted for 54.9%, and service fee revenue accounted for 1.2%; the overall value of B2C is higher. The proportion of revenue increased from 43% in 2018 to 55% in 2020.

The second method is to divide according to the cross-border trade, general trade and service fee models. According to the prospectus, the three models achieve revenues of 42.7%, 56.1%, and 1.2% respectively. Similarly, the gross profit margin is relatively low. The proportion of revenue generated by the high cross-border trade model has increased from 34% in 2018 to 43% in 2020.

The most direct result of the continuous optimization of the business structure is the continuous improvement of the company’s gross profit and gross profit margin, and the establishment of a relatively stable profitability. From 2018 to 2020, the gross profit margin of Youquhui is 24.3%, 28.9% and 31.7%, and the trend of continuous improvement is significant.

(Source: company prospectus)

According to the prospectus, Youquhui recorded a gross profit of 870 million yuan in 2020. According to statistics from 2018 to 2020, the company’s compound annual growth rate (CAGR) of gross profit reached 20.6%. The operating profit and adjusted net profit during the period can be steadily maintained at 140 million and 100 million or more respectively.

Based on the above, from the financial data, Youquhui has shown a good side, and it also has better performance data than comparable companies in the same industry. This is not only the advantage brought by the company’s scale effect, the author believes that it is also due to Brought by the company’s overall strength or the accumulated advantages formed by competitive barriers, as a leading enterprise in the FMCG brand e-commerce operation service track, Youquhui has demonstrated its “both offensive and defensive” in its latest prospectus. Characteristics, growth is also not lacking in certainty. Next, we will continue to expand our horizons and timeline, and look at the company’s investment value from a longer-term perspective.

Strong late-comer advantage, occupying a favorable position in the segmented track of brand e-commerce

As for the future growth space of Youquhui, it can be analyzed from its market position and service capabilities.

According to the information, Youquhui has a significant first-mover advantage in the cross-border field. It is not only the first batch of cross-border e-commerce operation service providers on Tmall International, and the first batch of e-commerce operation service providers to deploy warehouses in bonded areas, but also the first. Approved operation service providers responsible for Moony and Kobayashi brand Tmall International CIP (Centralized Import Procurement) innovation projects.

Youquhui has been awarded a five-star service provider on Tmall for many consecutive years, and it is also a purple star service provider on Tmall International. This is one of the few branded e-commerce service providers certified by China’s largest e-commerce platform. At present, Youquhui Operating 18 Tmall flagship stores and 26 Tmall international flagship stores.

In addition, Youquhui is also a member company of Jingdong Meili Alliance, and is a platform-certified beauty brand e-commerce service provider. According to the “Comprehensive Competitiveness Ranking List of Chinese Brand E-commerce Service Providers” recently released by the third-party data agency iiMedia Research, Youquhui was selected as one of the Top 15 Chinese Brand E-commerce Service Providers in Comprehensive Competitiveness, reflecting the company’s comprehensive strength and recent years The rapid growth is obvious to all in the industry.

According to the Insight Consultation report, Youquhui ranked first among Chinese branded e-commerce solution providers in terms of GMV of Japanese branded fast-moving consumer goods sold in China through e-commerce channels in 2019, with a market share of 5.5%.

(Source: company prospectus)

Currently, Youquhui operates 88 stores on major e-commerce platforms, providing a total of 28 brand partners and 66 brands with branded e-commerce solutions, of which 58 brands are from Japan.

Compared with general trade, cross-border trade is a breakthrough point for overseas brands to enter the Chinese market, especially for small and medium-sized brands, it is the most convenient choice for them to enter the Chinese market. Cross-border e-commerce supply often needs to coordinate multiple participants. Professional cross-border e-commerce solution providers like Youquhui continue to highlight their business advantages and can seize the opportunity of rapid market expansion.

According to reports from Zhuzhi Consulting and others, from 2014 to 2019, the market size of China’s imported brand e-commerce operation services increased to 559.2 billion yuan at a compound growth rate of about 40.2%. At the same time, the scale of this market is expected to continue to expand at a compound growth rate of about 8.2%, reaching 829.3 billion yuan by 2024. In the Japanese fast-moving consumer brand field focused on by Youquhui, the corresponding e-commerce service market has grown even faster, with approximately 43.1% from 2014 to 2019, and approximately 8.7% from 2019 to 2024.

(Source: company prospectus)

And it’s worth emphasizing that Based on data analysis, Youquhui also has outstanding brand marketing capabilities and content production capabilities.

Look at the data intuitively, The number of fans in all B2C flagship stores operated by Youquhui has exceeded 10 million Among them, the Sophie Tmall flagship store and Moony Tmall international flagship store have 3.3 million fans and 1.8 million fans respectively. In terms of content layout, Youquhui has established its own MCN agency Lido Culture, and incubates its own KOLs on e-commerce platforms such as Taobao, Xiaohongshu and Douyin.

Corresponding, Youquhui’s powerful new brand incubation capabilities cannot be ignored . Taking Gangwon Province as an example, using ECRP system and user behavior models to analyze and use data, Youquhui has successfully solved the challenges of low repurchase rate, low promotion efficiency, and unbalanced income structure faced by Gangwon Province’s new entry into the Chinese market. Successfully stimulated the stickiness of its brand users. Judging from the repurchase rate indicators of large domestic e-commerce festivals such as “Double 11”, the repurchase rate of Tmall international stores in Gangwon Province operated by the company has increased from 11% in 2018 to 29% in 2020.

Concluding part

In summary, the author judges that among the few powerful brand e-commerce service companies, Youquhui, which has differentiated competitive advantages, has the opportunity to break through and grow rapidly.

It is worth mentioning that Youquhui not only stands on the competitive track of cross-border e-commerce, fast-moving consumer products, and B2C e-commerce in the growth stage, but the company currently exhibits strong capabilities in capturing traffic, mining data, and marketing monetization. , And the new brand incubation capabilities generated by the platform that can comprehensively reflect the company’s integrated, omni-channel, high-value-added, and full-life-cycle e-commerce operation and comprehensive service capabilities, which provide a deep foundation for the company’s “late-mover advantage”. It is expected to accelerate the realization of the company’s ranking round and increase in influence in the industry. Therefore, the time of Youquhui’s listing fell above the critical point of the company’s new round of outbreak, which can be said to be in line with the law and trend of the development of things.

The menacing Youquhui will undoubtedly bring a lot of pressure on competing companies in the same industry, and even stimulate the entire branded e-commerce service industry to produce a similar “catfish effect”. The company’s continuous strengthening of the Internet platform’s “bilateral” “Network effect” is one of its important intrinsic values. With the deepening of the “moat”, Youquhui’s listing in Hong Kong is a good opportunity for it to continue to grow bigger and stronger. For investors, the same should not be done. Ignore such opportunities

You must log in to post a comment.