Monthly review:

41 domestically listed Chinese companies, 7 overseas listed Chinese companies, and the amount of IPO financing increased month-on-month.

36 Chinese companies are supported by VC/PE institutions, among which domestic listed companies account for 90%

JD Logistics received the highest IPO financing amount this month, and the logistics industry ranked first in financing amount

The number of listed companies in Guangdong Province remains the leading; Beijing and Shanghai have both raised over RMB 10 billion in financing

The China Securities Regulatory Commission will study and formulate a package of institutional measures to prohibit improper shareholding by resignees from the system to make up for the shortcomings of the system

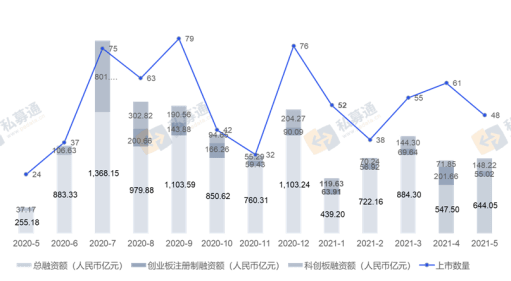

According to data from Zero2IPO Private Equity, there are 48 Chinese companies in May 2021[1]The number of IPOs completed in various global trading markets increased by 100% year-on-year; the total financing amount was 64.405 billion yuan, and the financing amount increased by 149.5% year-on-year and 17.6% month-on-month. Chinese companies that completed their IPO this month involved 16 primary industries and landed in 7 trading markets. The average IPO financing amount of Chinese companies was 1.342 billion yuan, an increase of 49.4% from the previous month. The highest single financing amount was 20.229 billion yuan. A total of 36 VC/PE-backed companies went public this month, involving 205 institutions, with a VC/PE penetration rate of 75%.

Figure 1 The number of domestic and overseas listings and total financing amount of Chinese companies from May 2020 to May 2021

Source: Private Equity Pass 2021.6 www.pedata.cn

The total financing amount of IPO companies in the top ten in May accounted for 69.1%

The three IPO companies with the largest amount of financing this month are: JD Logistics listed on the main board of the Hong Kong Stock Exchange, raising a total of 20.229 billion yuan; Hehui Optoelectronics listed on the Shanghai Stock Exchange Science and Technology Innovation Board, raising a total of 7.106 billion yuan; The Shanghai Stock Exchange was listed on the Science and Technology Innovation Board and raised a total of 2.901 billion yuan.

Table 1 Top 10 IPO corporate financing in May

Source: Private Equity Pass 2021.6 www.pedata.cn Table 2 Top 10 listed Chinese companies in financing supported by domestic and overseas VC/PE IPOs in May Source: Private Equity Pass 2021.6 www.pedata.cn Registered listed companies accounted for more than 50%, and the amount of overseas listed financing increased month-on-month In May, there were 41 domestic listed Chinese companies, accounting for 85.4% of the number of Chinese companies IPO this month. The initial financing amounted to 39.646 billion yuan, accounting for 61.6% of the total financing for the month. In May 2021, 11 and 14 companies were successfully registered and listed on the Growth Enterprise Market and the Science and Technology Innovation Board, accounting for 52.1% of the total number of listed companies in the month, and initial financing accounted for 31.6%. In May, 4 Chinese concept stocks were listed on the U.S. stocks, with a financing amount of approximately RMB 3.093 billion; 3 companies were listed on the main board of the Hong Kong Stock Exchange, with a financing amount of approximately RMB 21.666 billion. The amount of financing in the U.S. and Hong Kong stock markets both increased from last month. Figure 2 Distribution of domestic and overseas listings of Chinese companies in May 2021 (by listing sector) Source: Private Equity Pass 2021.6 www.pedata.cn Figure 3 The distribution of Chinese companies listing in the domestic market under different IPO systems from May 2020 to May 2021 Source: Private Equity Pass 2021.6 www.pedata.cn Guangdong Province leads the way in the number of IPOs, and Beijing ranks first in terms of financing According to private equity statistics, in May 2021, the number of IPOs in the five provinces and cities of Guangdong, Jiangsu, Shanghai, Zhejiang and Beijing is 5 or more, a total of 32; the initial financing amount plus a total of RMB 50.99 billion, accounting for the country The total amount is nearly 80%. Among them, Guangdong Province leads other provinces in the number of listings of 9 Chinese companies; Beijing and Shanghai have raised financing amounts of more than 10 billion yuan respectively, and Beijing ranked first in the amount of financing raised by Chinese companies listed at 24.988 billion yuan, accounting for about 38.8%. Table 3: Geographical distribution of Chinese companies’ domestic and overseas listings in May 2021 Source: Private Equity Pass 2021.6 www.pedata.cn The May IPO involved 16 industries, with the logistics industry having the highest amount of financing In May 2021, the IPO will involve 16 industries. The number of listed companies in machinery manufacturing, biotechnology/medical health, chemical raw materials and processing industries is 5 or more. In terms of financing, the logistics industry IPO financing was 21.09 billion yuan, accounting for 32.8% of the total financing of Chinese enterprises, ranking first; semiconductor, electronic equipment, and machinery manufacturing industries ranked second and third respectively, with financing amounts exceeding 7 billion. yuan. Figure 45: Industry distribution of the number of IPO companies and financing amount in month 45 Source: Private Equity Pass 2021.6 www.pedata.cn The VC/PE penetration rate of listed companies in May was 75% Among the listed companies this month, 36 Chinese companies were supported by VC/PE institutions, of which 33 were listed domestically, accounting for 91.7%. There are 7 and 13 IPO companies on the ChiNext Board of the Shenzhen Stock Exchange and the Science and Technology Innovation Board of the Shanghai Stock Exchange, respectively, which have received support from VC/PE institutions. The book returns of VC/PE-invested companies listed on domestic listings have dropped. In May 2021, the book return multiples (calculated at issue price) were 1.96 times, a decrease of 27.4% from the previous month and a year-on-year decrease of 35.1%; the book returns of overseas listings in May 2021 increased significantly year-on-year , An increase of 97.21%. Figure 5 Trend of VC/PE-backed IPO penetration from May 2020 to May 2021 Source: Private Equity Pass 2021.6 www.pedata.cn Figure 6 Distribution of book returns of VC/PE supporting IPOs in domestic and overseas markets of Chinese companies from May 2020 to May 2021 (issuance date) Source: Private Equity Pass 2021.6 www.pedata.cn 16 VC/PE institutions have won no less than 2 Chinese IPOs Among the listed companies this month, 36 Chinese companies received support from VC/PE institutions, a decrease of 12.2% from the previous month. Among them, 16 institutions have invested companies with no less than 2 IPOs. The book return of Lieliang Fund in the Waterdrop IPO was as high as 98.26 times. Table 45 Listed in VC/PE Institution Invested Companies (Partial Institutions) Source: Private Equity Pass 2021.6 www.pedata.cn Note: 1. The IPOs listed in the above table refer to companies headquartered in China (excluding Hong Kong, Macao and Taiwan) that are first listed on domestic and foreign stock exchanges within the scope of the statistics in 2021. Companies listed in the second listing and multiple listings are not listed. Included; 2. The investment institution only lists the named shareholders appearing in the prospectus; 3. The book amount is the number of shares held by the institution before the initial issuance of the invested project (excluding the cornerstone wheel/strategic placement) * issue price It is calculated that part of the book value may be biased because the number of shares held before the IPO was not disclosed in the prospectus. The China Securities Regulatory Commission issued the Guidelines for the Supervision of the Shareholding Behavior of Retired Persons from the Securities Regulatory Commission System, clarifying the verification requirements for the participation of the resigned employees The China Securities Regulatory Commission has always attached great importance to the supervision of shareholders of companies to be listed, continuously improved the shareholder supervision system and mechanism, and made great efforts to prevent illegal and illegal “creation of wealth”. In February of this year, the China Securities Regulatory Commission issued the “Guidelines for the Application of Regulatory Rules Regarding Information Disclosure of Shareholders of Listed Companies Applying for Initial Public Offerings”, which strengthened the regulatory constraints on surprise share purchases, abnormal share prices, transfer of interests, and “shadow shareholders”, and compacted the information of companies to be listed. Disclosure responsibility and intermediary agency verification responsibility to guide legal and compliant investment in companies that are to be listed. During the implementation of the system, the China Securities Regulatory Commission insisted on cutting its blade inward, and simultaneously studied and formulated a package of system measures to prohibit improper shareholding by system resignees to make up for the shortcomings of the system. While strengthening anti-corruption supervision and management and improving the independent review system, we have specially formulated and issued the “Guidelines for the Application of Regulatory Rules Issuance No. 2” (hereinafter referred to as the “Guidelines”) to clarify that the retired personnel of the China Securities Regulatory Commission will participate in the public offering and listing or the New Third Board. The verification requirements of selected-tier listed companies highlight the targeted supervision of resigners who fall within the scope of the specification, compact the verification responsibilities of intermediary agencies, and maintain the “three public” order in the market. The “Guidelines” mainly include the following: One is to clarify the circumstances of improper shareholding. The resignation personnel of the CSRC system used the influence of their original position to seek investment opportunities, the process of shareholding has the transfer of interests, the shareholding during the shareholding prohibition period, the shareholding as an unqualified shareholder, the source of the shareholding funds violates laws and regulations, etc., are considered to be improper shareholding. The second is to strengthen the verification responsibilities of intermediary agencies. In the process of verifying shareholder information, intermediary agencies should comprehensively check whether there is a shareholding situation of resigned personnel specified in the Guidelines and determine whether it is an improper shareholding situation. In the case of improper share purchase, it shall be cleared up. When the issuer and the intermediary institution submit the application documents for the issuance and listing (listing), they shall make a special explanation on the relevant verification status of the resigned personnel of the CSRC system. After submitting an application for issuance and listing (listing), if an improper shareholding situation is discovered or a major media question arises, the intermediary institution shall check and report in a timely manner. The third is to strengthen audit supervision and establish an independent review system. Review the issuance and listing (listing) review process involving the participation of departed employees to ensure that the review process is fair, just, and in compliance with laws and regulations. If clues of violations of law and discipline are found, they shall be handed over to relevant departments for handling. Key case analysis of this month: JD Logistics, Hehui Optoelectronics, Electric Wind Power JD Logistics is listed in Hong Kong, and another listed company is added to the JD department On May 28, 2021, JD Logistics officially listed on the Hong Kong Stock Exchange under the stock code of “02618.HK”. It is the second listed company incubated by JD Group. JD Health has been listed on the Hong Kong Stock Exchange before this. The issue price of JD Logistics is HK$40.36 per share per share, and it plans to issue 60,160,800 shares, with a market value of approximately RMB 202.294 billion. On the day of issuance, the closing price was HK$41.7, and the net proceeds from the IPO were approximately HK$24.113 billion. JD Logistics is a technology-driven supply chain solution and logistics service provider under JD. It was born out of JD Group’s self-built logistics. In 2012, it officially registered a logistics company. In 2017, JD Logistics Group was established. On February 16, 2021, JD Logistics submitted a prospectus on the Hong Kong Stock Exchange and officially launched the IPO. Three months later, JD Logistics officially launched a global public offering of shares. JD Logistics’ IPO has attracted attention from many parties. On May 20, JD Logistics’ IPO subscription ended ahead of schedule. JD Logistics was subscribed by more than 1 million people, oversubscribed by more than 700 times, and frozen funds exceeded 550 billion Hong Kong dollars. According to data from the JD Logistics prospectus, in 2018, 2019 and 2020, JD Logistics’ revenues were 37.9 billion yuan, 49.8 billion yuan, and 73.4 billion yuan, respectively. Among them, there was a year-on-year increase of 31.6% in 2019 and a year-on-year increase of 47.2% in 2020, almost compared to 2018. Doubled. In the first quarter of 2021, JD Logistics’ revenue reached 22.4 billion, a year-on-year increase of 64.1%, and continued to maintain rapid growth. At the same time, JD Logistics already has profitability. According to previously disclosed public data, after excluding changes in fair value such as equity incentives that do not affect the company’s value, JD Logistics has a profit of more than 1.7 billion in 2020. Source: Private Equity Pass 2021.6 www.pedata.cn Display panel manufacturer Hehui Optoelectronics goes public, with an issue market value of RMB 35.529 billion On May 28, 2021, Hehui Optoelectronics “688538.SH” was listed on the Science and Technology Innovation Board of the Shanghai Stock Exchange with an issue price of 2.65 yuan per share. It plans to issue 2.681 billion shares, with a total financing amount of 7.106 billion yuan and a market value of 35.529 billion yuan. . The closing price on the day of listing was 4.2 yuan, with a turnover of 6.441 billion yuan. The controlling shareholder of Hehui Optoelectronics is Lianhe Investment. Before this issuance, Union Investment held a total of 8.05 billion shares of the company, accounting for 75.12% of the company’s total share capital. The actual controller of the company is the Shanghai State-owned Assets Supervision and Administration Commission, which holds 100% equity of Lianhe Investment. Hehui Optoelectronics is a well-known AMOLED semiconductor display panel manufacturer in China, focusing on the R&D, production and sales of small and medium-sized AMOLED semiconductor display panels. According to the prospectus, Hehui Optoelectronics has focused on small and medium-sized AMOLED since its establishment. It is the first domestic manufacturer to achieve mass production of AMOLED semiconductor display panels in the industry, breaking the foreign monopoly. At present, Hehui Optoelectronics has two production lines of the 4.5th generation and the 6th generation, both of which can produce rigid and flexible AMOLED panels. Among them, the production capacity of the 4.5th generation AMOLED production line is 15K/month, the planned production capacity of the 6th generation AMOLED production line is 30K/month, and the mass production capacity is 15K/month, and the 15K/month production capacity is expected to be mass-produced in the second quarter of this year. However, although Hehui Optoelectronics believes that the future growth rate of flexible AMOLED is better than that of rigid AMOLED, it is also known that the flexible display scene has not yet appeared on a large scale, so it is still mainly based on rigid AMOLED. Hehui Optoelectronics’ rigid AMOLED panel mass production capacity ranks first in China and second in the world, while the revenue of flexible products in 2020 is only 71,500 yuan. Source: Private Equity Pass 2021.6 www.pedata.cn “The first share of state-owned assets split” electric wind power successfully listed on the Science and Technology Innovation Board of the Shanghai Stock Exchange On May 19, 2021, Shanghai Electric Wind Power Group Co., Ltd. “688660.SH” was listed on the Science and Technology Innovation Board of the Shanghai Stock Exchange, with an issue price of 29.01 yuan per share, 533 million shares issued, and a market value of 7.253 billion yuan. According to the announcement, about 2.901 billion yuan of raised funds will be invested in “new product and technology development projects”, “Shanghai Electric Wind Power Group Shandong Haiyang Test Base Project”, “post-market capability improvement project” and other projects, and Reasonably arrange capital investment. Electric Wind Power was established in 2006 and is a holding subsidiary of Shanghai Electric Group Co., Ltd. As the first state-owned company to split a listed stock, in June last year, Electric Wind Power submitted a listing application to the China Securities Regulatory Commission. After nearly a year, it successfully listed on the Science and Technology Innovation Board. At present, the company’s products cover a full range of wind turbines from 1.25MW to 8MW, basically achieving full power coverage. In addition, the company firmly grasps the major development trends of industry refinement, customization, and large megawatts, and conducts active product development and layout in the onshore 4.X series, 5.X series and the offshore 5.X series and 8.0MW series. . In addition to the overall design technology of wind turbines, the company also has the core technology research and development capabilities of wind turbines represented by blade technology and control technology, and has formed technical research and development capabilities and advantages in key components and key technologies

You must log in to post a comment.